Physical Address

304 North Cardinal St.

Dorchester Center, MA 02124

Physical Address

304 North Cardinal St.

Dorchester Center, MA 02124

Africa’s upstream sector is being told that everything is finally going its…

In April, Uber's chief technology officer told The Information that the company had spent its entire 2026 artificial intelligence budget. It was four months into the year. Nobody had misused anything. Engineers had used Claude Code for precisely the work it was built to do: parallel agent execution, large scale refactoring, automated test generation. Praveen Neppalli Naga reported burning $1,200 in a single two hour session during a personal demo of the tool.

Korea's fertility rate went up. Two years running. Births in 2025 came in at 254,457, a 6.8 percent increase on the prior year, and the total fertility rate lifted from 0.75 to 0.80. Headlines followed. Officials made careful noises about a turning point. Somewhere in a ministry building, a paper is being drafted that says the policy finally worked.

Every investment thesis built on artificial intelligence rests on a single unproven claim: that the technology raises output per worker enough to justify the capital being poured into it. The evidence offered for that claim is almost always the same evidence. A company announces it is cutting staff. It attributes the cut to AI. The market treats the announcement as proof that the productivity gain is real and bankable.

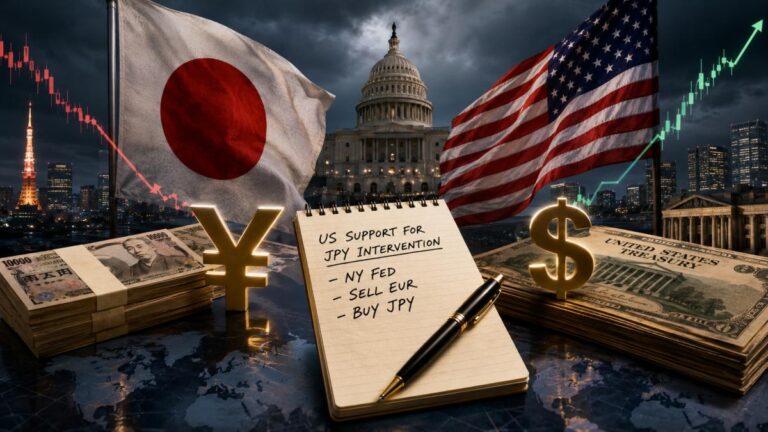

On Friday, July 31, a Reuters photographer captured an image over the shoulder of US Treasury Secretary Scott Bessent during a cabinet meeting at Camp David. On the notepad in front of him, under his own name card, were two lines: "To Do," followed by "Buy Japanese Yen (JPY) $5-10 bil." Hours later, the Financial Times reported that the New York Fed had sold euros to buy yen on the Treasury's behalf....

Every quarter brings a fresh round of headlines about German carmakers drowning. The framing is always the same: three proud industrial giants, battered by Chinese competition and American tariffs, fighting to keep their heads above water. It makes for good copy. It is also about two years out of date.

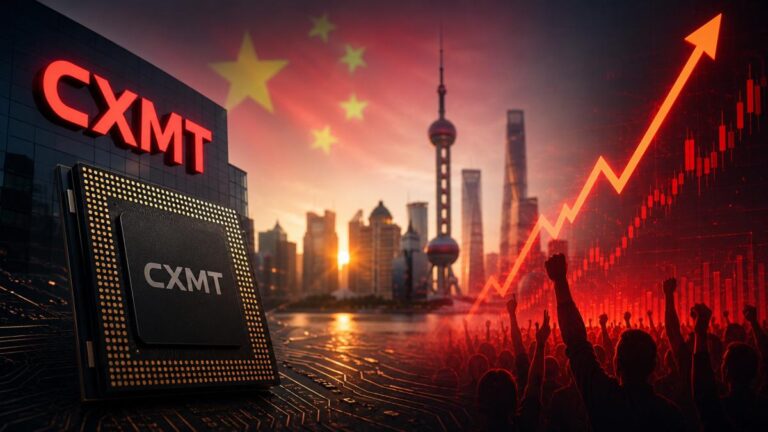

The story the market told itself on 27 July was simple enough. China's largest memory manufacturer came to market, raised a fortune, and immediately became a threat to the three companies that have run the DRAM industry for two decades. Micron fell. Samsung fell. SK Hynix fell. The narrative wrote itself before anyone had finished reading the prospectus.

Ask a hundred people why they own clean energy stocks and you will get a hundred variations on the same answer. Decarbonisation is inevitable. Solar is now the cheapest electricity in history. Governments have committed trillions. The technology curve only points one way.

The bear case on artificial intelligence has completed its journey from contrarian to consensus, and almost nobody has noticed what that transition costs. When a position is held by career Treasury analysts, the Bank for International Settlements, the ratings agencies, a large share of financial media and roughly every second post on investment social media, it has stopped being an insight. It has become the ambient mood. Arguing that the AI trade is overextended in mid 2026 is not a call. It is a description of the weather.

There is a story circulating in energy circles that goes roughly like this. The Middle East is on fire, crude is in the high eighties after touching triple digits, the Strait of Hormuz has been throttled for months, and the obvious escape hatch is sitting right there in plain sight. Solar modules cost nine cents a watt. Sodium-ion batteries just entered mass production. Surely, if the crisis grinds on for another year or two, the world simply routes around the barrel.