Physical Address

304 North Cardinal St.

Dorchester Center, MA 02124

Physical Address

304 North Cardinal St.

Dorchester Center, MA 02124

When a reactor stock triples in a week, every retail investor on the planet starts asking the same question: is it too late to buy? That question, while understandable, tends to obscure a far more interesting one hiding underneath it. The reactors generating all the excitement cannot operate without a very specific type of fuel. That fuel is barely being produced domestically anywhere in the Western world. And the bottleneck it represents may be one of the most compelling supply-side stories in the energy sector right now.

The headline-chasing crowd is staring at reactor stocks. The contrarian case points somewhere else entirely.

The electricity problem driving this entire thesis is not speculative. It is already showing up in grid planning documents, utility earnings calls, and congressional testimony. Data center energy consumption in the United States grew from roughly 76 terawatt hours in 2018 to 176 terawatt hours in 2023, representing approximately 4.4 percent of total national electricity use. By 2028, that figure is projected to land somewhere between 325 and 580 terawatt hours, or between 6.7 and 12 percent of national electricity consumption, according to analysis published by the Belfer Center for Science and International Affairs at Harvard.

That is not a modest increase. That is a near-doubling of demand from a single sector in under five years. And it arrives at a moment when the grid is already stressed, interconnection queues are multi-year backlogs, and the political pressure to avoid blackouts is intensifying.

Small modular reactors have emerged as one of the most discussed responses. Unlike utility-scale nuclear plants that take a decade to permit and build, SMRs are designed for factory assembly and faster deployment. They can be co-located with data centers, bypassing the transmission constraints that make grid-based power increasingly unreliable. The International Energy Agency has tracked a pipeline of conditional offtake agreements between SMR developers and data center operators growing from 25 gigawatts at the end of 2024 to 45 gigawatts more recently. The interest is real and it is accelerating.

In late 2025, the U.S. Department of Energy selected TVA and Holtec Government Services to receive up to 800 million dollars in cost-shared federal funding for the first utility-scale SMR deployments in American history. TVA plans to build a GE Vernova Hitachi BWRX-300 at the Clinch River site in Tennessee. Holtec is targeting two SMR-300 units at the Palisades site in Michigan. Secretary of Energy Chris Wright called it the start of America’s nuclear renaissance.

The stock market responded to this story, and reactor developers were bid aggressively higher. That reaction is entirely rational as a statement about the long-term direction of the sector. It becomes less rational when examined against a simple timeline: neither project is expected to deliver electricity before the early 2030s. Investors pricing these companies for a 2025 cash flow reality are buying a 2032 story at a 2025 valuation.

This is not new behavior. Growth investors have a long track record of paying peak multiples for projects that slip, run over budget, and encounter regulatory friction before they ever generate a dollar of revenue. The history of large infrastructure projects suggests this pattern will repeat.

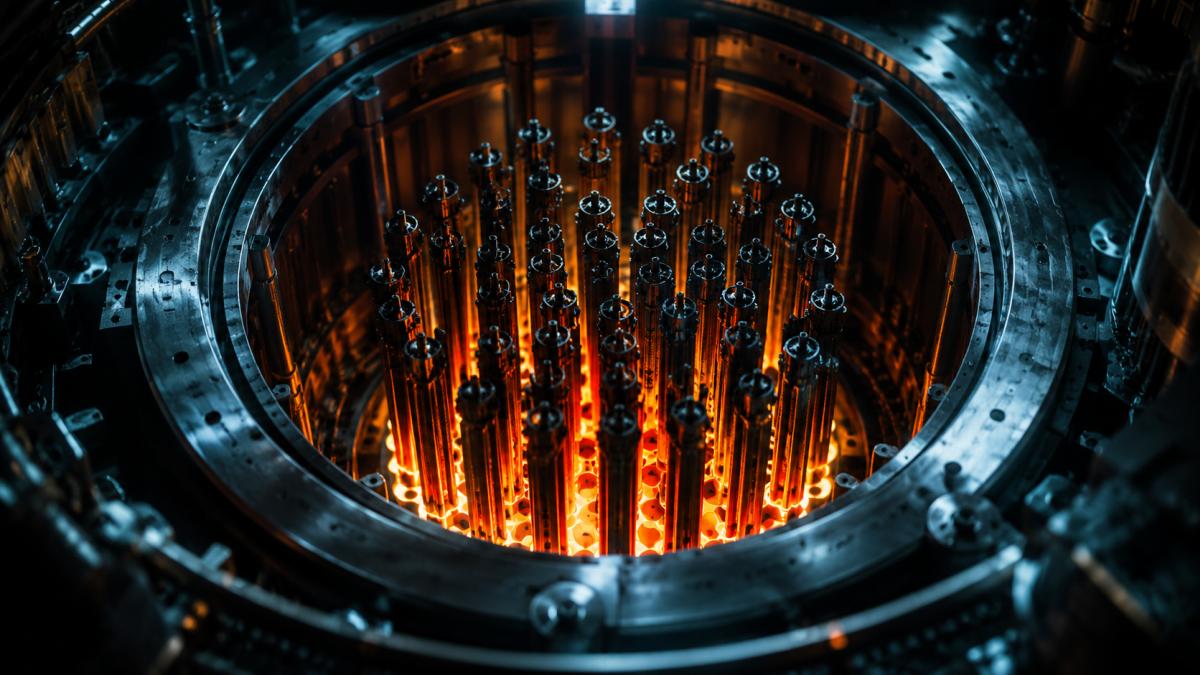

Here is the part of the narrative that receives almost no mainstream coverage. The next generation of advanced reactors, including the designs now receiving federal backing, do not run on the same low-enriched uranium that powers the existing U.S. fleet. They require a specialized fuel called HALEU, which stands for high-assay low-enriched uranium. HALEU is enriched to between five and twenty percent uranium-235, placing it well above the three to five percent enrichment typical of conventional reactor fuel, but well below weapons-grade material.

Without a domestic HALEU supply chain, none of these reactors can operate at commercial scale. The fuel must exist before the reactors can be commissioned. And right now, the United States produces almost none of it.

The dependency problem runs deeper than most investors realize. Russia’s state-owned enrichment infrastructure, operating under Tenex and its parent Rosatom, historically supplied roughly 27 percent of U.S. enriched uranium demand and controlled nearly half of global enrichment capacity. In May 2024, the Biden administration signed the Prohibiting Russian Uranium Imports Act into law, which mandates a full ban on Russian uranium imports by January 2028 and unlocked 2.72 billion dollars in previously authorized funding to rebuild a domestic supply chain. Russia responded with its own temporary export restrictions. The supply chain rupture is in motion.

The question is who fills the gap.

There is exactly one publicly traded company operating an NRC-licensed HALEU production facility on U.S. soil. Centrus Energy, trading on NYSE American under the ticker LEU, runs the American Centrifuge Plant in Piketon, Ohio. In June 2025, Centrus completed the delivery of 900 kilograms of HALEU to the Department of Energy, finishing Phase II of its DOE contract and immediately entering Phase III with an extension valued at approximately 110 million dollars through mid-2026. The DOE retains options for up to eight additional production years beyond that date.

The structural advantage Centrus holds is regulatory rather than technological. Building and licensing a uranium enrichment facility in the United States takes years, involves extensive NRC oversight, and carries significant capital requirements. No competitor is waiting in the wings with a licensed, operating cascade ready to scale. When the DOE needs to write a large check for domestic HALEU production, the addressable pool of capable vendors is very short.

The Centrus story is not without risk. Its near-term revenue is heavily contract-dependent, the DOE holds significant discretion over whether future options get exercised, and the stock already carries a meaningful premium on the expectation of continued government engagement. But the underlying logic is clean: the government has a legally mandated fuel independence problem, the infrastructure to solve it is scarce, and Centrus controls the most advanced piece of that infrastructure currently in operation.

[Also See: Falling for Private Investment Scams]

This is a picks-and-shovels position in the classic sense. The gold prospectors of the 1850s largely went broke. The merchants selling them equipment did not.

Before enrichment happens, uranium must be mined. The United States imports more than ninety percent of its uranium requirements. Rebuilding a domestic supply chain from scratch takes time, but several smaller producers have been quietly ramping up output against a favorable policy backdrop.

UR Energy, listed as URG, operates the Lost Creek in-situ recovery mine in Wyoming and recently commenced initial production at its second site, Shirley Basin. The company launched mining operations at Shirley Basin in April 2025, describing it as bringing a historically significant uranium district back to life. At full production across both sites, UR Energy targets up to 2.2 million pounds of uranium per year. The company has locked in long-term offtake contracts with U.S. utilities, converting production output into contracted revenue rather than pure spot market exposure.

The risk profile here is meaningfully different from Centrus. URG is a small-cap name with a tight float and significant daily price volatility. It amplifies uranium price movements rather than smoothing them. Investors who understand that dynamic and size positions accordingly are accessing pure-play domestic uranium exposure with a credible production story already in motion.

For those seeking institutional-grade exposure to the same macro theme with less single-stock volatility, Cameco (CCJ) remains the most liquid option. As the largest publicly traded uranium producer in the Western world, Cameco owns the MacArthur River Mine in Canada, which holds the highest-grade uranium deposit on Earth, and holds a 49 percent stake in Westinghouse, positioning it directly across both the fuel and reactor design segments of the nuclear supply chain. CCJ is the position that pension funds and large asset managers use to build nuclear exposure. It will not triple in a quarter, but it also will not collapse on a single earnings miss.

The conventional trade in nuclear right now is to buy the reactor story. The contrarian trade is to recognize that reactors are long-dated, politically sensitive, and perpetually subject to delay. The fuel supply chain, by contrast, is a current problem being addressed with current government contracts and current production ramp-ups.

Centrus is being paid today. UR Energy is shipping uranium today. Cameco is signing long-term contracts with utilities that need fuel certainty regardless of what happens to any individual reactor project.

This is the difference between a story stock and a cash flow story. The sector narrative may be the same, but the risk-adjusted return profile across these two categories of investment looks very different when examined closely. For readers building a longer-term thesis around the nuclear energy cycle, the fuel supply chain deserves at least as much attention as the reactor developers generating the headlines.

This article does not constitute financial advice. All investments carry risk and readers should conduct their own due diligence before making any investment decision. For more analysis on contrarian energy themes, explore related coverage at Market Mind Investor.