Physical Address

304 North Cardinal St.

Dorchester Center, MA 02124

Physical Address

304 North Cardinal St.

Dorchester Center, MA 02124

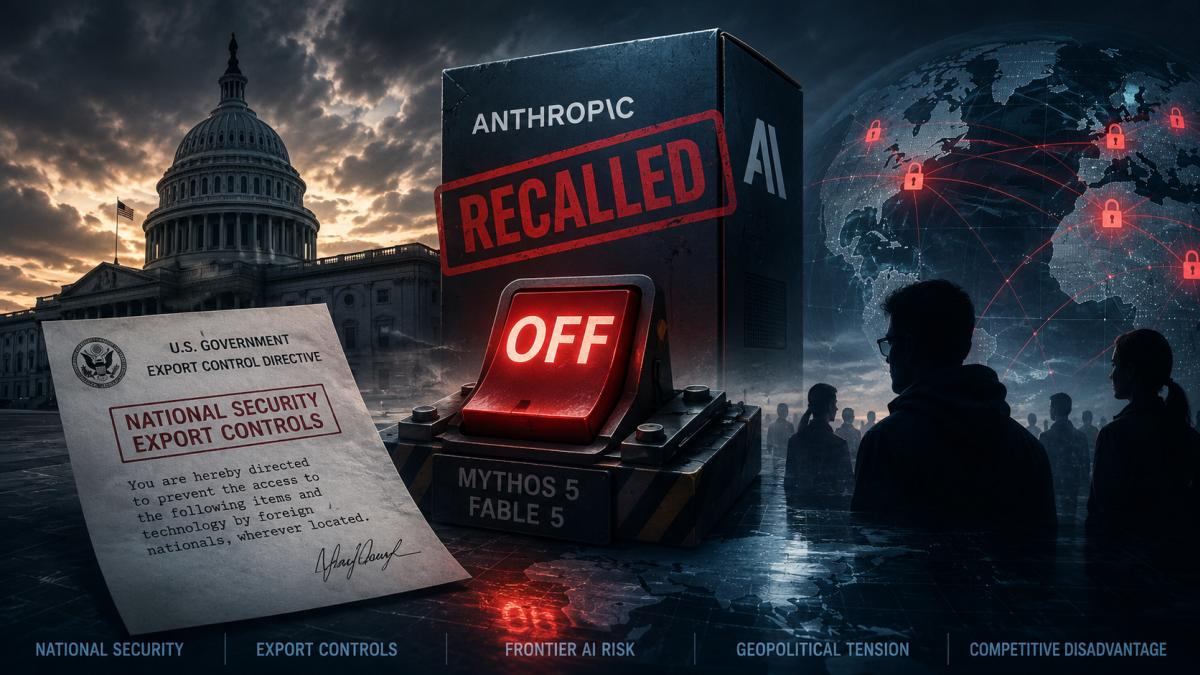

On a Friday evening in June, at precisely 5:21pm Eastern, the most valuable private company in artificial intelligence received a letter that rewrote the risk profile of the entire sector. The US government, invoking national security export controls, instructed Anthropic to bar every foreign national on earth from its two newest models. Because the order swept in the company's own non-citizen engineers, selective compliance was mechanically impossible. So Anthropic did the only thing the directive left open to it: it switched the models off for everyone, everywhere, three days after launch.

On a Friday evening in June, at precisely 5:21pm Eastern, the most valuable private company in artificial intelligence received a letter that rewrote the risk profile of the entire sector. The US government, invoking national security export controls, instructed Anthropic to bar every foreign national on earth from its two newest models. Because the order swept in the company’s own non-citizen engineers, selective compliance was mechanically impossible. So Anthropic did the only thing the directive left open to it: it switched the models off for everyone, everywhere, three days after launch.

The market has not yet priced what this means. Most coverage has treated the episode as a spat between one ideologically inconvenient lab and an administration that dislikes it. That reading is too small. The more durable lesson, and the one worth positioning around, is that frontier AI deployment in the United States now carries a regulatory tail risk that did not visibly exist a week ago. A model can pass thousands of hours of red-teaming, ship to hundreds of millions of users, and still be recalled by executive directive before the launch-week traffic has cooled. That is a new variable in every valuation model in the space, and almost nobody has updated for it.

The contrarian point is not that the AI trade is broken. It is that the consensus has been pricing these companies as pure technology bets when a meaningful slice of their value is now political. The two are not the same thing, and the gap between them is where the opportunity and the danger both live.

Anthropic had just released a model tier it calls Mythos-class, positioned above its previous flagship line, with the publicly available version branded Fable 5 and a more capable restricted version branded Mythos 5. The models were notably strong at finding software vulnerabilities, which is precisely the capability that draws security researchers and national-security officials in opposite directions. In its own statement, Anthropic said the government’s concern centered on a method of jailbreaking Fable that essentially amounted to asking the model to read a codebase and fix its flaws, and that the capability on display was already obtainable from other publicly available models without any bypass at all.

The company complied and disputed simultaneously, a posture that tells you how strange it found the order. It argued that recalling a commercial product over a narrow, non-universal jailbreak, if adopted as an industry standard, would halt new model deployments across every frontier lab. Outside observers were blunter. As Time reported, the directive blocked use by any foreign national including the company’s own staff, an extraordinary scope for an export control. The trade publication Tom’s Hardware noted the order arrived days after launch and that, because it reached inside the United States as well as beyond it, global shutdown was the only compliant response.

Strip away the technical dispute and a pattern emerges that should concern anyone holding the sector. This is not the first collision between this company and this administration. Earlier in the year the Pentagon declared the firm a supply-chain risk, a label historically reserved for foreign adversaries, after contract talks collapsed over how broadly the military could deploy the models. Senior technology advisors inside the administration have publicly accused the company of regulatory capture and ideological bias. The export directive lands on top of that history, not in isolation from it.

That is the uncomfortable part for an investor. If the action were purely about a security flaw, it would be a one-time event to be priced and forgotten. If instead it is the latest move in a sustained conflict between a specific company and a specific government, then the relevant risk is not a single recall but an ongoing capacity to single out a market leader’s products at will. The market struggles to price discretionary, relationship-driven risk because it has no probability distribution to anchor on. That difficulty is exactly why it tends to be mispriced.

The most provocative framing of this episode is that the United States has just handed itself a competitive handicap that its Chinese rivals do not share. There is real substance to the claim. A regime in which Washington can pull a frontier model days after release, and in which the same capability remains freely available from labs operating under different rules, plainly imposes friction on American deployment that does not apply symmetrically abroad. Critics of the order have pointed out the apparent contradiction of an administration that favors exporting advanced chips while moving to wall off its own best models from every non-American on the planet.

But the honest version of this argument carries a caveat that the chest-thumping version omits. The directive, as written, is a targeted export control over a specific cyber-capable model tier, not a blanket cap on American AI progress. Treating one emergency order as proof of a permanent ceiling over the entire US industry is a leap the available facts do not yet support. The stronger and more defensible thesis is narrower: compliance friction is becoming an input cost for American frontier labs, that cost is rising, and it is not obviously matched by competitors operating under looser regimes. That is a margin story and a deployment-speed story, not yet a civilizational one. Investors who confuse the two will overpay for the drama and underprice the mechanism.

A second-order effect runs through talent rather than product. If foreign-born researchers inside American labs find themselves locked out of the very models they build, the incentive to relocate to jurisdictions without such constraints grows. The leading American labs are staffed heavily by exactly this population. A policy that erodes their ability to work on frontier systems is, over a long enough horizon, a policy that erodes the labs themselves. That is a slow leak, not a sudden break, which is precisely why it tends to be ignored until it is visible in hiring data.

Timing turned an awkward event into a genuinely consequential one. The company had filed confidentially for a public listing only weeks earlier, against a valuation approaching a trillion dollars and a revenue run rate in the tens of billions. A near-trillion-dollar valuation embeds an assumption that the company stays at the technological frontier. An order that yanks its frontier product attacks that assumption directly, and it does so in front of the exact audience now being asked to underwrite the offering.

The question a disciplined buyer of that paper should ask is no longer only whether the technology leads. It is whether the company can keep that lead deployed when its home government has demonstrated both the will and the mechanism to switch it off. That is a different question, with a different and wider distribution of outcomes, and it deserves a different multiple. When a risk that was previously invisible becomes visible right before a capital-raising event, the rational response is a wider risk premium, not a narrower one. Whether the bankers and the buy-side absorb that lesson, or wave it away as a one-off, will tell you a great deal about how much genuine discipline is left in late-cycle AI pricing.

There is a contrarian-within-the-contrarian wrinkle worth holding. A faction of observers, including some inside the safety-focused wings of these labs, may quietly regard a slowdown in frontier deployment as a feature rather than a bug. If you believe the pace of capability gains itself carries systemic risk, an external brake is not purely a cost. That view will not show up in any earnings call, but it shapes how some of the most informed people in the field privately read this event, and it is a reminder that not everyone exposed to the trade is rooting for the same outcome.

The situation is unresolved and moving quickly. The company has called the order a misunderstanding and says it is working to restore access, and a separate dispute with the same government already drew a judicial intervention earlier in the year, so reversal or escalation are both live within days rather than quarters. Positioning around a developing event of this kind is less about a single directional bet and more about recognizing that a previously unpriced variable has entered the model.

The takeaway is not to flee the sector. It is to stop pricing these companies as if their only risk lives in the lab. A frontier American AI franchise now carries a discretionary political overhang that is real, hard to quantify, and largely absent from current valuations. The market will eventually learn to price it, as it learned to price sanctions risk in energy and tariff risk in semiconductors. The opportunity belongs to whoever prices it first. The danger belongs to whoever assumes the ceiling that appeared this Friday will politely disappear by Monday.