Physical Address

304 North Cardinal St.

Dorchester Center, MA 02124

Physical Address

304 North Cardinal St.

Dorchester Center, MA 02124

Imagine standing at the edge of a swimming pool, watching the water ripple as people jump in and out. Some dive straight in without hesitation, hoping they won’t land in the deep end. Others dip their toes cautiously, testing the waters before taking the plunge. Now think about investing—it’s a lot like that pool. Some people want to dive in headfirst, risking the chance of hitting choppy waters, while others wish for a steadier, more predictable approach.

If you’ve ever worried about making that big investment splash at the wrong moment, you’re not alone. The stock market can feel like a rollercoaster—rising one day and plunging the next. The question for many new investors is always the same: Is this the right time? What if there was a way to swim safely without the fear of whether the water is too hot or too cold? That’s where Dollar-Cost Averaging (DCA) steps in—a method that lets you wade into the investment pool gradually, without worrying about catching the perfect wave.

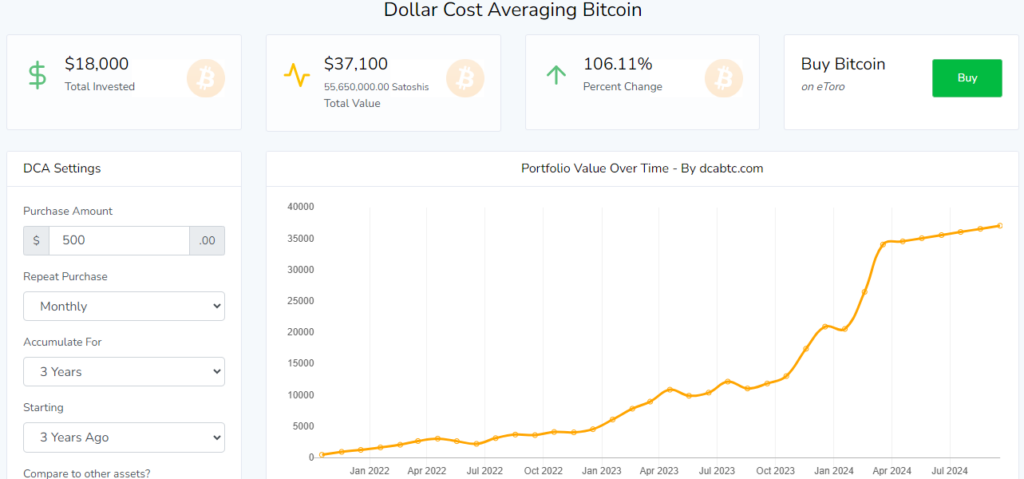

Below is an example of what your growth would like if you had dollar cost averaged $500 per month over the last 3 years in Bitcoin. Investing a total of $18,000 would have yielded a total value of $37,100.

In this guide, we’ll demystify the strategy behind DCA, showing how it can keep your investment stress levels low and your portfolio afloat, regardless of the market’s ups and downs. We’ll walk you through its benefits, limitations, and real-life examples, helping you become a more confident investor in the process.

Let’s start with a story: Meet Alex. Every month, Alex gets a paycheck, and a small portion of that paycheck goes directly into an investment account—no questions, no overthinking. Whether the stock market is soaring or tumbling, Alex invests the same amount each month, buying shares of a mutual fund. Some months, that $500 buys a little more because prices are low, and some months, it buys less because prices are high. But over time, Alex’s average cost per share evens out.

This, in a nutshell, is Dollar-Cost Averaging (DCA).

It’s like grocery shopping with a fixed budget. Some weeks, apples are on sale and you can get a whole bagful. Other weeks, the price spikes, and your $10 only buys a handful. By consistently buying apples every week, though, you’re never overpaying across the long run, and you’re never missing out on the savings when prices dip.

DCA is built on the idea that you don’t have to time the market perfectly to succeed. You don’t have to predict when stocks will hit rock bottom or peak prices. Instead, you smooth out the ups and downs by committing to invest the same amount on a regular schedule, whether the market is up, down, or somewhere in between.

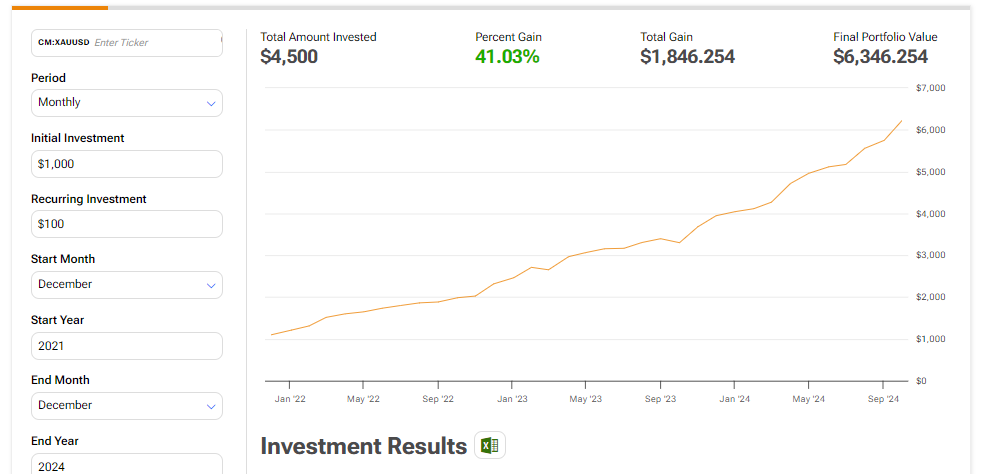

Below is a dollar cost average illustration of gold over the last 3 years

Just like Alex, you can use DCA to keep emotions out of investing—no more staring at charts, wondering if today is the best time to invest. With DCA, every day is a good day to invest because the strategy is built around consistency and discipline, not trying to outguess the market’s next move.

DCA isn’t about getting rich quick, but it’s about getting rich steadily. It’s the financial equivalent of running a marathon rather than sprinting. It helps you stick to a plan, one step at a time, without worrying about tripping on market dips.

Real Examples: Dollar-Cost Averaging in Action

To really understand the power of Dollar-Cost Averaging, let’s walk through a simple example of how this strategy plays out over time—both in good markets and bad.

Let's say Sarah wants to invest in an S&P 500 ETF, and she has decided to invest $400 monthly for 5 months. Here's how DCA plays out in real market conditions:

Month 1 (Market Price: $100/share)

Invests: $400

Buys: 4 shares

Average cost per share: $100

Month 2 (Market Price: $80/share)

Invests: $400

Buys: 5 shares

Average cost per share: $89.33 ($800/9 shares)

Month 3 (Market Price: $120/share)

Invests: $400

Buys: 3.33 shares

Average cost per share: $98.77 ($1200/12.33 shares)

Month 4 (Market Price: $90/share)

Invests: $400

Buys: 4.44 shares

Average cost per share: $96.51 ($1600/16.77 shares)

Month 5 (Market Price: $110/share)

Invests: $400

Buys: 3.64 shares

Average cost per share: $98.93 ($2000/20.41 shares)

Final Results:

Total invested: $2,000

Total shares owned: 20.41

Average cost per share: $98.93

Market value at end: $2,245.10 (20.41 shares × $110)

Return: +12.26%

Key Observations:

When prices dropped in Month 2, Sarah automatically bought more shares

When prices rose in Month 3, she bought fewer shares

Her average cost ($98.93) ended up being lower than the final share price ($110)

She never had to time the market or make emotional decisions

This is why DCA is often called "emotional insurance" - it removes the stress of trying to time the market perfectly.

Now let’s dig into why Dollar-Cost Averaging is like a trusty compass for navigating the unpredictable seas of investing. Imagine you’re sailing through a storm—waves crashing, winds howling, and no clear view of what’s ahead. Without a compass, you might make wild guesses about which direction to go, and you could end up anywhere, maybe even in worse trouble. But with DCA, you’re sailing steady. No matter how wild the market gets, you’re guided by consistency, knowing you’ll reach your destination in time.

DCA’s biggest advantage? It helps smooth out the turbulence. By investing the same amount of money at regular intervals, you’re naturally buying more shares when prices are low and fewer when they’re high. This lowers your average cost over time. It’s a great buffer against volatility. Think of it as spreading out your risk, like planting seeds in different seasons rather than all at once. Some seeds will bloom in the spring, others in the fall—but in the end, you’ll have a healthy garden.

DCA works best for those with a long-term view. If you’re saving for retirement, college, or your dream home, this strategy allows you to build wealth gradually over time without getting caught up in the short-term market noise. It’s like planting a tree—you won’t see immediate growth, but over the years, those consistent investments will bear fruit.

DCA is a powerful tool, but like any tool, it works best in certain situations. Imagine you’re trying to hang a picture. A hammer works perfectly for a nail, but you wouldn’t use it to tighten a screw, right? The same goes for DCA—it’s most effective in particular market conditions.

When the market’s on a rollercoaster ride, DCA is like the harness that keeps you safe. In volatile markets, where prices swing up and down, DCA allows you to buy more shares when prices are lower and fewer when they’re higher. It takes the stress out of these wild fluctuations, ensuring that you’re not making risky, emotional decisions based on short-term panic or euphoria.

If your goal is to invest for the long haul, DCA is your best friend. Over time, the highs and lows of the market tend to average out, and DCA ensures that you’re steadily building a portfolio without worrying about the perfect entry point. Think of it like filling a piggy bank—you add a little bit consistently, and one day you’re surprised at how much it’s grown.

DCA is ideal for those with regular income streams who want to invest smaller, manageable amounts. If you have $500 to invest monthly, for example, DCA is a perfect way to grow your portfolio over time without worrying about dumping a large sum in all at once and wondering if you got the timing right.

But let’s not put on rose-colored glasses just yet. Like any strategy, DCA has its limitations.

If the market is in a continuous upward trend, lump-sum investing might outperform DCA. In this case, spreading out your investments means you could miss out on some of the gains you would have earned by investing everything up front. It’s like watching a train leave the station without you because you’re only boarding one car at a time.

Making regular investments means you could incur more transaction fees, especially if your platform isn’t commission-free. This might seem like pennies at first, but over time, those costs can eat into your returns. It’s like paying for extra tickets every time you board the train instead of getting a single pass.

DCA isn’t a get-rich-quick strategy. It requires patience. The rewards are long-term, so if you’re someone who expects fast results, this approach might test your resolve. It’s much like planting a tree—you won’t see the fruits of your labor immediately, but over time, that steady growth will pay off.

So, what’s the final takeaway? Dollar-Cost Averaging is the tortoise in the race against the hare. It’s steady, it’s consistent, and it doesn’t get thrown off course by the wild pace of market highs and lows. Whether you’re new to investing or looking for a way to simplify your strategy, DCA offers a reliable path to building wealth without the stress of market timing.

At the end of the day, the beauty of DCA lies in its simplicity. You don’t need to be a market guru or possess perfect timing to see success. All it takes is a plan, some discipline, and a commitment to your long-term goals. With DCA, the market’s ups and downs become background noise, and your focus shifts to what really matters: investing steadily and letting time do the work for you.

So, what’s stopping you from starting your DCA journey? It’s time to take that first step—no matter the size of the waves ahead.