Physical Address

304 North Cardinal St.

Dorchester Center, MA 02124

Physical Address

304 North Cardinal St.

Dorchester Center, MA 02124

What many traditional financial advisors won't tell you is that "playing it safe" with bonds and annuities can actually be risky in its own way. While these investments might protect you from market volatility, they expose you to a different, more subtle danger: the steady erosion of your purchasing power through inflation.

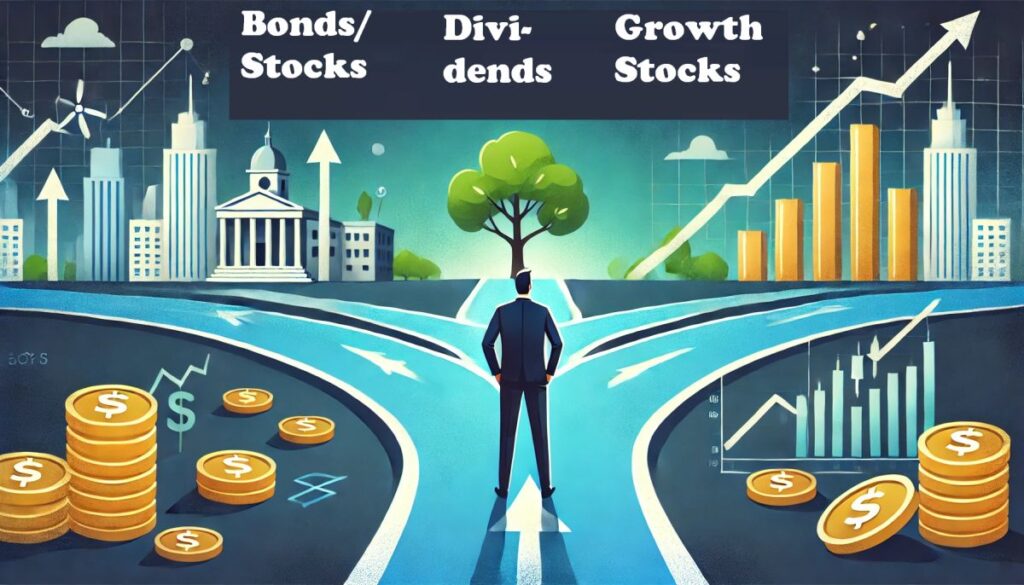

Picture this: You’re standing at a crossroads of investment opportunities, each path promising to lead you toward financial security. To your left, there’s a well-worn path of traditional bonds and savings accounts – familiar, but perhaps not as rewarding as they once were. To your right, there’s the exciting but often volatile world of growth stocks. But right in front of you stands a path that many successful investors have quietly taken for decades: dividend-paying stocks.

I remember when I first discovered the power of dividend stocks. Like many investors, I had started my journey chasing the next big thing – hopping from one trending stock to another, always looking for that elusive massive gain. It wasn’t until I watched my neighbor, retired comfortably at 60, explain how his dividend portfolio had not only weathered multiple market storms but actually grown stronger through them, that I truly understood the potential of this investment approach.

Today, we’re going to explore how dividend-paying stocks could potentially help you beat the market while building a reliable income stream. We’ll examine why traditional “safe” investments might not be as secure as they seem, especially when inflation enters the picture, and why dividend stocks might offer a compelling alternative.

Think of bonds and annuities as being like a boat anchored in a harbor. At first glance, they appear stable and secure. However, what many investors don’t realize is that the water level (purchasing power) is constantly changing due to inflation, and that sturdy anchor might actually be holding you back.

Let’s say you invest $100,000 in a 10-year government bond paying 4% annually. Sounds safe, right? But here’s where the story takes an unexpected turn. If inflation runs at 3% (close to the historical average), your “real” return is only 1%. In higher inflation environments, like what we’ve seen recently, your supposedly “safe” investment could actually be losing purchasing power every year.

Think of it this way: If you kept $100 in a shoebox for ten years and inflation averaged 3% annually, that $100 would only buy about $74 worth of goods at the end of that period. Bonds work similarly – while the nominal value of your investment stays stable, its real-world purchasing power can be quietly eroding.

[Dividend Stocks Versus Bonds In 2024 | Which Is Better?]

Annuities present a similar challenge, but with additional complexities. Imagine signing a contract to receive $3,000 monthly for life. Sounds great until you realize that $3,000 won’t buy the same basket of goods in 20 years that it does today. If inflation averages 3%, that $3,000 payment would have the equivalent purchasing power of about $1,650 in 20 years.

Beyond the inflation risk, annuities often come with:

What many traditional financial advisors won’t tell you is that “playing it safe” with bonds and annuities can actually be risky in its own way. While these investments might protect you from market volatility, they expose you to a different, more subtle danger: the steady erosion of your purchasing power through inflation.

This is where dividend-paying stocks enter the picture. Unlike bonds with fixed payments, quality dividend-paying companies can increase their payouts over time, potentially helping investors stay ahead of inflation. But before we dive into how dividend stocks can help beat the market, it’s crucial to understand that this isn’t about abandoning bonds and annuities entirely – it’s about understanding their limitations and finding a better balance for long-term growth.

Imagine planting a tree that not only grows taller each year but also produces seeds that you can plant to grow more trees. That’s essentially how dividend growth and reinvestment works. Let me share a story that illustrates this perfectly.

A few years ago, I met Sarah, a retired teacher who had started investing in dividend-paying stocks in her early 30s. She began with just a few shares of Johnson & Johnson, a well-known dividend aristocrat. “The initial dividend payments seemed so small,” she told me, “hardly enough for a nice dinner out.” But Sarah did something crucial: she reinvested every dividend payment to buy more shares.

[Recommended book: Dividend Growth Machine – Nathan Winklepleck]

Thirty years later, her initial $10,000 investment had transformed into a substantial nest egg that was generating more in quarterly dividends than her original investment. This isn’t just Sarah’s story – it’s a demonstration of the power of dividend growth investing done right.

Think of dividend growth like a raise at work. Just as your salary should increase over time to keep pace with your growing experience and inflation, quality dividend-paying companies typically raise their dividend payments annually. This isn’t just good news for investors – it’s often a signal of corporate health and confidence in future earnings.

Consider these aspects of dividend growth:

Here’s where the real wealth-building potential comes into play. When you reinvest dividends, you’re essentially creating a powerful feedback loop. Let me break this down with a simplified example:

Year 1:

You own 100 shares at $50 each ($5,000 investment)

Company pays 3% dividend ($150 annual dividends)

Reinvesting buys you 3 new shares

Year 2:

You now own 103 shares

Company raises dividend by 7%

Your dividend income increases from both:

More shares owned

This compounding effect is like a snowball rolling downhill, gathering size and momentum as it goes. The key is consistency and patience. As Warren Buffett once said, “The stock market is a device for transferring money from the impatient to the patient.”

Let's put some real numbers behind this concept. Consider a company paying a 3% dividend yield with a modest 6% annual dividend growth rate. An initial $10,000 investment, with dividends reinvested, could potentially grow to:

$21,000 after 10 years

$44,000 after 20 years

$92,000 after 30 years

And these figures don’t include potential capital appreciation of the underlying shares. The beauty of this system is that it works while you sleep – no constant monitoring or trading required.

Not all dividend-paying companies are created equal. The best ones share certain characteristics that make them particularly effective wealth-building tools. Think of these companies as mighty oak trees rather than fast-growing but fragile saplings.

The foundation of any great dividend-paying company is a robust business model. Imagine a castle built on solid bedrock versus one built on sand. Companies with strong business models typically have:

Take a company like Procter & Gamble, for instance. People need household products regardless of economic conditions, and strong brand loyalty allows them to maintain healthy profit margins even during challenging times.

A company’s financial health is like a person’s physical fitness – it needs consistent maintenance and disciplined habits. The best dividend-paying companies typically demonstrate:

I once interviewed a CFO of a major dividend-paying corporation who explained it perfectly: “We run this company like we’re preparing for a marathon, not a sprint. Every financial decision we make considers not just next quarter’s results, but our ability to reward shareholders consistently for decades to come.”

This might be the most underappreciated aspect of successful dividend-paying companies. The best ones view their shareholders as business partners, not just investors. This commitment typically manifests in:

Take companies like the Dividend Aristocrats – those that have increased their dividends for at least 25 consecutive years. This isn’t just about having enough money to pay dividends; it’s about fostering a corporate culture that prioritizes shareholder returns.

As we conclude our deep dive into dividend investing, let’s focus on the most crucial aspect of potentially beating the S&P 500: identifying and investing in companies that consistently increase their dividend payouts. This strategy isn’t just about finding high yields – it’s about finding growing yields.

Several excellent resources can help you identify companies with strong dividend growth histories:

For investors who prefer a more hands-off approach, several funds specialize in dividend growth investing:

These funds offer instant diversification and professional management, though they come with expense ratios that should be considered.

[15 Companies that have paid dividends for more than 100 years]

Whether you choose individual stocks or funds, focus on these key principles:

Remember, successful dividend growth investing isn’t about finding the highest current yield – it’s about finding reliably increasing dividends. A company paying a 2% yield but growing it by 10% annually can be more valuable long-term than one paying 4% with no growth.

The key to beating the market with dividend stocks lies in this growth component. While the S&P 500 might offer higher short-term returns at times, a well-constructed portfolio of dividend growers can potentially provide:

Before making any investment decisions, consider consulting with a financial advisor to ensure your strategy aligns with your goals and risk tolerance. Whether you choose individual dividend growth stocks or specialized funds, the most important factor is maintaining a long-term perspective and allowing the power of growing dividends to work in your favor.

After all, the ultimate goal isn’t just to match the market – it’s to build a reliable, growing income stream that can support your financial future while potentially delivering market-beating returns along the way.

Remember: The best time to plant a tree was twenty years ago. The second best time is now. The same principle applies to building your dividend growth portfolio.

Note to Readers: Investment returns cannot be guaranteed, and past performance doesn’t indicate future results. Always conduct thorough research and consider seeking professional financial advice before making investment decisions.