Physical Address

304 North Cardinal St.

Dorchester Center, MA 02124

Physical Address

304 North Cardinal St.

Dorchester Center, MA 02124

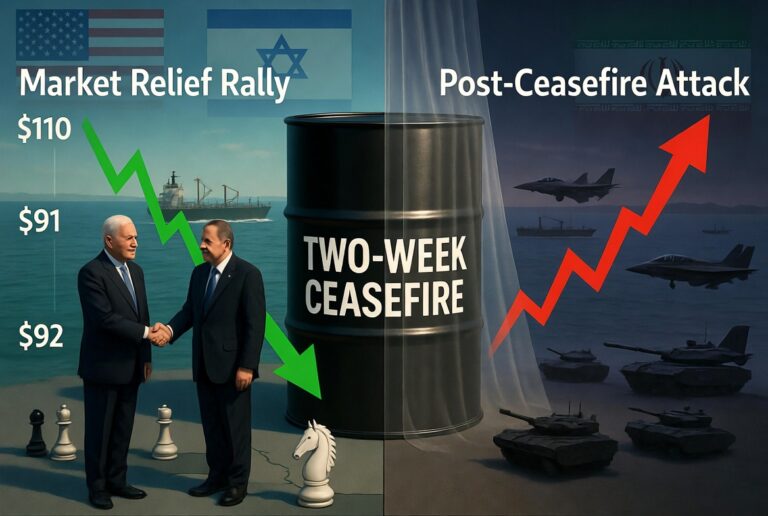

The global landscape has shifted dramatically as military conflicts escalate and international tensions reach levels not seen in decades. What was once promised as an era of diplomacy has transformed into a period marked by aggressive territorial actions and proxy conflicts spanning multiple continents. For investors, this reality demands a fundamental reassessment of portfolio construction and risk management strategies.

The global landscape has shifted dramatically as military conflicts escalate and international tensions reach levels not seen in decades. What was once promised as an era of diplomacy has transformed into a period marked by aggressive territorial actions and proxy conflicts spanning multiple continents. For investors, this reality demands a fundamental reassessment of portfolio construction and risk management strategies.

When geopolitical stability crumbles, traditional investment approaches often fail to protect wealth. The correlation between asset classes tends to increase during crisis periods, meaning diversification alone may not provide adequate protection. Understanding defensive investing becomes not just prudent but essential for capital preservation.

History demonstrates that military conflicts create distinct economic patterns. Government spending surges, supply chains face disruption, commodity prices become volatile, and currencies can experience rapid devaluation. The U.S. Federal Reserve historically responds to such environments with accommodative monetary policy, though current inflationary pressures complicate this traditional playbook.

During the World Wars, Korean conflict, and Vietnam era, specific sectors dramatically outperformed while others languished. Defense contractors, energy producers, and precious metals showed resilience when broader markets struggled. Today’s conflicts, though different in nature, create similar dynamics that astute investors can position themselves to weather.

The psychological dimension matters equally. Market participants react to headlines, escalations, and peace negotiations with emotional volatility that creates both risk and opportunity. As explored in perspectives on collective consciousness during global crises, mass psychology during wartime generates fear-based decision making that often proves counterproductive for long-term wealth building.

The most obvious beneficiaries of sustained military conflict are defense contractors and aerospace manufacturers. Companies producing weapons systems, military aircraft, naval vessels, and cybersecurity solutions see order books expand when governments prioritize security spending. Major defense primes like Lockheed Martin, Northrop Grumman, and Raytheon Technologies have historically delivered strong returns during periods of elevated military expenditure.

However, defense investing carries complexities. Government contracts operate on long cycles, margins face political scrutiny, and ethical considerations weigh on some investors. The sector also tends to underperform during peace dividends when military budgets contract. Timing matters significantly.

Beyond traditional defense manufacturers, cybersecurity firms represent a modern dimension of military preparedness. Nations increasingly recognize digital infrastructure as critical as physical borders, driving sustained investment in protection against cyber warfare, espionage, and critical infrastructure attacks.

Military conflicts disrupt global energy flows and commodity supply chains, creating price spikes that benefit producers. Oil and natural gas companies positioned in politically stable regions gain pricing power when supplies from conflict zones become uncertain. The energy sector historically shows negative correlation with broader equity markets during geopolitical stress.

Precious metals serve as the ultimate defensive assets. Gold has preserved wealth through every major conflict of the modern era. When currencies face debasement through wartime spending and investors flee riskier assets, gold consistently attracts capital flows. Silver follows similar patterns with added industrial demand that can amplify moves.

Agricultural commodities deserve attention as food security becomes strategic priority during extended conflicts. Disruptions to major grain-producing regions, fertilizer supply constraints, and export restrictions can drive dramatic price increases. Companies with farmland holdings, agricultural equipment manufacturers, and fertilizer producers position themselves at critical supply chain nodes.

The World Gold Council provides comprehensive data on gold’s performance during various historical crisis periods, demonstrating its consistent role as a monetary hedge when political and economic stability comes into question.

Despite concerns about sovereign debt levels, U.S. Treasury securities remain the global benchmark for safety during periods of extreme uncertainty. When equity markets sell off aggressively and investors prioritize capital preservation over returns, Treasury bonds attract enormous flows. This dynamic holds especially true for short to intermediate duration securities that minimize interest rate risk.

The paradox of wartime Treasury investing is that the very government issuing the bonds may be funding massive military expenditures through deficit spending, yet investors continue viewing these instruments as safe havens. This reflects the dollar’s reserve currency status and the absence of credible alternatives at comparable scale and liquidity.

Investment-grade corporate bonds from defensive sectors provide another avenue for stability-focused portfolios. Companies in utilities, consumer staples, and healthcare typically maintain strong balance sheets and predictable cash flows that support debt service even during economic downturns triggered by geopolitical events.

Electric utilities, water companies, and natural gas distributors operate essential infrastructure with regulated returns and minimal exposure to economic cycles. Consumers continue requiring electricity and water regardless of whether bombs are falling overseas. These characteristics make utilities attractive defensive holdings, particularly those paying consistent dividends that provide income during market turbulence.

Consumer staples companies selling food, beverages, household products, and personal care items demonstrate similar resilience. Procter & Gamble, Coca-Cola, and Walmart serve needs that persist through recessions and conflicts. While these stocks may not deliver explosive growth, their stable earnings and cash generation protect capital when growth sectors correct sharply.

The International Monetary Fund regularly publishes analysis on how various economic sectors perform during crisis periods, providing empirical backing for defensive sector positioning.

Military conflicts often trigger currency volatility as capital flees unstable regions and seeks perceived safety. The U.S. dollar typically strengthens during global crises despite America’s own fiscal challenges, simply because alternatives appear worse. However, overconcentration in any single currency creates risk.

Swiss francs, Singapore dollars, and Norwegian krone represent currencies backed by strong institutions, sound fiscal management, and limited military entanglements. Diversifying currency exposure through foreign bonds, international dividend stocks, or direct currency positions can hedge against potential dollar weakness if geopolitical dynamics shift unpredictably.

Emerging markets require careful analysis during wartime environments. Some nations benefit from commodity exports or strategic positioning, while others face capital flight and currency collapse. Selectivity matters enormously in international allocation during volatile periods.

Defensive investing during periods of military conflict requires balancing immediate protection against the reality that wars eventually end and markets recover. Overdefensive positioning means missing rebounds when peace negotiations succeed or conflicts reach stalemate. Historical data from MSCI shows that equity markets have recovered from every major military conflict, though timing varies significantly.

The optimal approach combines genuine defensive holdings that preserve capital during acute stress with selective positions in quality companies trading at crisis valuations. This balanced stance protects against worst-case scenarios while maintaining upside participation when sentiment improves.

Dollar-cost averaging into defensive positions prevents the common mistake of going all-in at market peaks after fear has already priced in significant risk. Systematic accumulation during volatility builds positions at attractive levels while maintaining liquidity for opportunities that emerge as situations evolve.

The current environment demands vigilance, flexibility, and emotional discipline. As conflicts intensify and diplomatic solutions prove elusive, investors who recognize the patterns of wartime economics and position accordingly stand better chances of not just surviving but potentially thriving through this challenging period. The key lies in acknowledging reality without succumbing to panic, maintaining strategic focus while remaining tactically nimble.